Quickbooks is a popular tool for small business owners. You can manage your books, track your spending, view your profits and more all within the easy-to-use interface. Today we want to talk about one feature the majority of users might not know about: reconciling.

Reconciling your finances is a practice carried over from old-school accounting, when professionals had to manually compare your check book to your bank statements to make sure all the numbers were accurate. Today, technology helps us out. Small businesses can reconcile their finances in Quickbooks in as few as three clicks to ensure accuracy, remove redundancies, and get the most up to date picture of their financial health.

What is Reconciling?

Reconciling is the process of ensuring that your business financial records match your bank statements. This can be incredibly important because it helps you track your spending and earnings. In business, you might see thousands of dollars coming in and out of your accounts every day. It can be tricky to keep track of all that money on your own. Reconciling those charges against your most recent bank statement can show you how much money you have for the coming month. But what does that process look like?

Before financial applications and bookkeeping software, you needed a CPA to help you with reconciling your books. It was time consuming and detailed work. Today, however, Quickbooks makes it easy for accountants and business owners alike to reconcile finances.

Quickbooks works by linking with your bank account to show you money coming in and out. With this in mind, some people argue you don’t need to reconcile because it’s all synced up. Not so. We can’t forget that technology isn’t flawless. Too often connections between Quickbooks and your bank can get interrupted and the two will stop communicating. If you regularly reconcile your finances, you’ll notice this disconnect quickly.

How Hard Is It to Reconcile in Quickbooks?

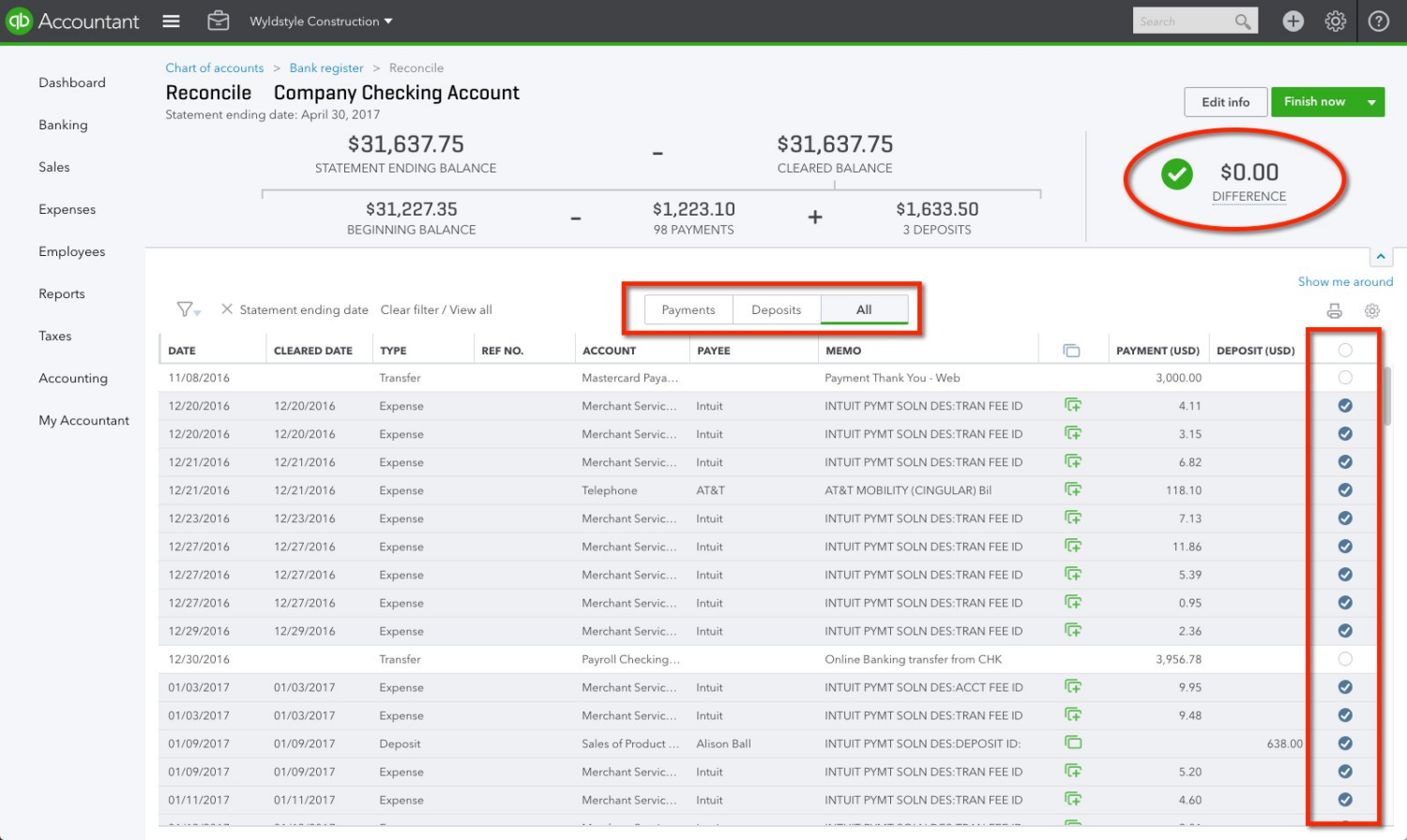

Reconciling within Quickbooks is as easy as entering the date of your most recent bank statement and the ending balance it shows in your account. Run the Quickbooks “reconcile” feature and it’ll show you things like your cleared balance, approved payments, the difference in your accounts and more. It’s a quick and easy way to make sure all of your financial records are accurate.

If you work with a CPA or accountant, odds are they’ll perform this task for you. It’s great to have professional assistance, but you still have a part to play in reconciliation. Sending over your bank statements to your accountant in a timely manner can help them reconcile your account more often, which makes the process quicker and your finances more accurate month to month or quarter to quarter.

How Often Should I Reconcile?

Reconciling frequently is important not only to check for accuracy and keep Quickbooks in sync with your bank, but also for basic business functions. Your reconciled account balance is the measurement CPAs will use to approve your books. They’ll use this number to estimate your taxes, make business projections, and even defend your business against the IRS if necessary.

The most common issue most people face with reconciliation is that they simply don’t do it often enough. If your books aren’t reconciled against your bank statements, you can never be 100% certain of how much you’re spending or making. This could result in overspending or holding on to money that could be invested. As a rule of thumb, it’s typically advised to reconcile your books at the end of each quarter, at the least. At the end of each month is ideal.

Why Does It Matter?

This might sound like a lot of work to add to your plate that frequently, but for small businesses, reconciling can make a big difference. Reconciled books are the “stamp of approval” that you’ve properly audited your financial records against bank and credit statements. It’s the first thing a CPA will look for when you go to them for help and can convince them you’re a safe bet to work with.

Not only does it help your CPA have confidence in your business skills, but it’s also a critical part to tax planning and preparation. Your tax information is all based on your finances, so if you aren’t sure how much you made or what you’re spending on, it can be tough to get the right return. If your tax professional has to go back and reconcile everything at year end, it’ll probably end up costing you more for their time. If you’ve been keeping track of reconciling, however, it could save you money with your CPA and increase the likelihood of a larger return.

How to Reconcile in Quickbooks

Reconciling in Quickbooks is a painless process. The software makes each step straightforward and the program doesn’t take long to crunch your numbers.

- Go to the banking tab on the left sidebar menu.

- Choose the account you’re going to reconcile.

- Process any open transactions that haven’t been imported to Quickbooks yet. These are the ones that do not have a blue check mark in the far right column.

- Go to the accounting tab in the left sidebar.

- Choose “Reconcile” from the pop-up menu.

- Choose the account you’d like to reconcile.

- A small form will appear. Using your most recent bank statement, input the ending balance and the date of the statement.

- Click “Start Reconciling.”

- Quickbooks will show you a spreadsheet of all your transactions since the last reconciliation and what charges still need to be reconciled. It also has a snapshot summary of your account at the top of the page.

Tips and Reminders for Reconciling in Quickbooks

Even with user-friendly processes, managing your finances in Quickbooks can still be more than you bargained for. If you’re managing your books on your own, the biggest thing to look out for is losing connectivity with your bank. If your Quickbooks becomes disconnected, reconnect it as soon as possible. The longer it stays out of sync with your bank, the larger risk you run of having to fix problems and input charges manually.

If you’re reading this and have never reconciled your finances or it’s been quite a while since you did, you might feel overwhelmed by the task ahead. Don’t worry. It’s all in your approach. Instead of trying to reconcile your entire business month by month, start with just one account. Reconciling each account individually makes the process smoother and reduces your risk of mistakes.

Ensure Accuracy In Your Finances

Reconciling in Quickbooks is an easy way to get a real-time picture of your finances. Syncing with your bank statements can make the process much easier than traditional manual methods, but make sure to check your connection frequently.

Working with a professional accountant can make the process even easier! Here at Every Single Bean, we have an experienced team who can help you manage your finances, boost your profits, and routinely reconcile your books. Schedule a call with us today!